Setting Budget & Why They Are Important

If absent a budget, the popularly referred to statement of “if you can’t measure it, you cannot manage it” is very true.

It’s often adapted further in the workplace to “without data, you’re just another person with an opinion”. True indeed.

A budget can be an intimidating reality of managing our lives, but it doesn’t have to be. The above commonly referred to statements are built on something that has some truth to it. All legends are built on some kernel of truth, right? Therefore, we acknowledge it and move forward with a plan.

Let’s get some misconceptions about them out of the way:

1) Budgets don’t have to complicated (we are not preparing them for a fortune 500 company in this case)

2) Templates are available everywhere, are often free to use, and are simple to complete

3) They are not 100% set in stone unlike common perceptions

- They can be tweaked, modified, or can give you directional input as needed

- There are acceptable levels of variance that can be adopted (i.e., +/- 10%)

- They are less restrictive than you think

4) You won’t be able to spend money on things that you enjoy or make you happy

- You absolutely can spend money on what you want, but you should budget for it!

5) I don’t need a formal budget, I do it all in my head

- If you can track all incoming and outgoing expenses, and that they are in line with your budget allocations, then you are a complete whiz, and should be working with our government to fix our national budget issues!

Let’s break each of these areas down one by one and explore them a little further to round out our discussion.

Budgets do not have to be complicated. Nor do you have to be an expert in math or have a finance degree to put one in place. They are available free online and all you need to do is plug is what is relevant to you, and your specific earnings and expenses.

Let’s break down how budgets are constructed to understand this better:

1) A simple way to look at a budget consists of three components

- Total income

- Total expenses

- How the expenses are categorized

How all the above computes each month is how you are doing against your budget. If it is favorable, you are managing your budget correctly. If negative, you are overspending, and the categorizations of expenses will show you just where the problem is.

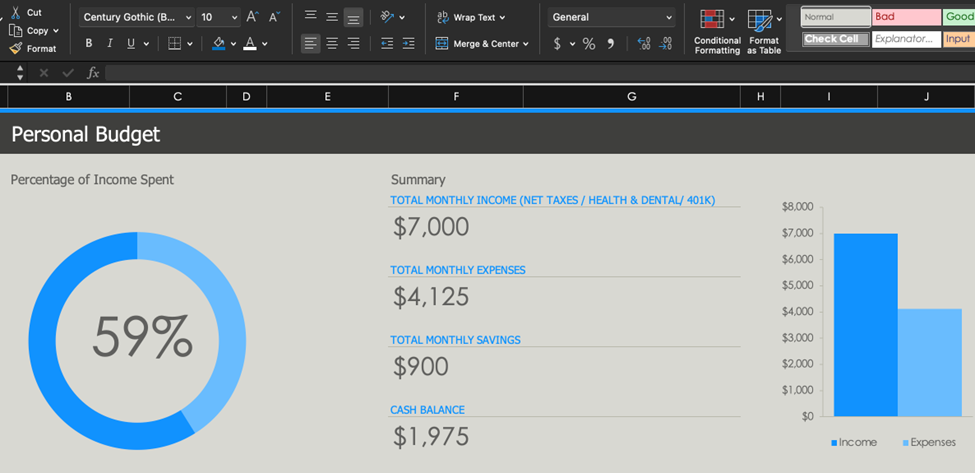

Let’s look at the below screen shot from my free budget template offered under the “resources” page on this site:

In this example, we are just looking at the 1st and 2nd components of a budget (the aggregates; total income and total expenses, and at a summary level, how they stack up).

We can clearly see here that total monthly expenses are short of total income, and thus, we are saving a certain amount of that each month and having cash left over (Cash Balance). This is a favorable position.

NOTE: These amounts are not purported to suggest that this should be your income versus spending, or that you should be saving this amount. Rather, it is merely illustrative to make it easy for you to understand the general concept involved.

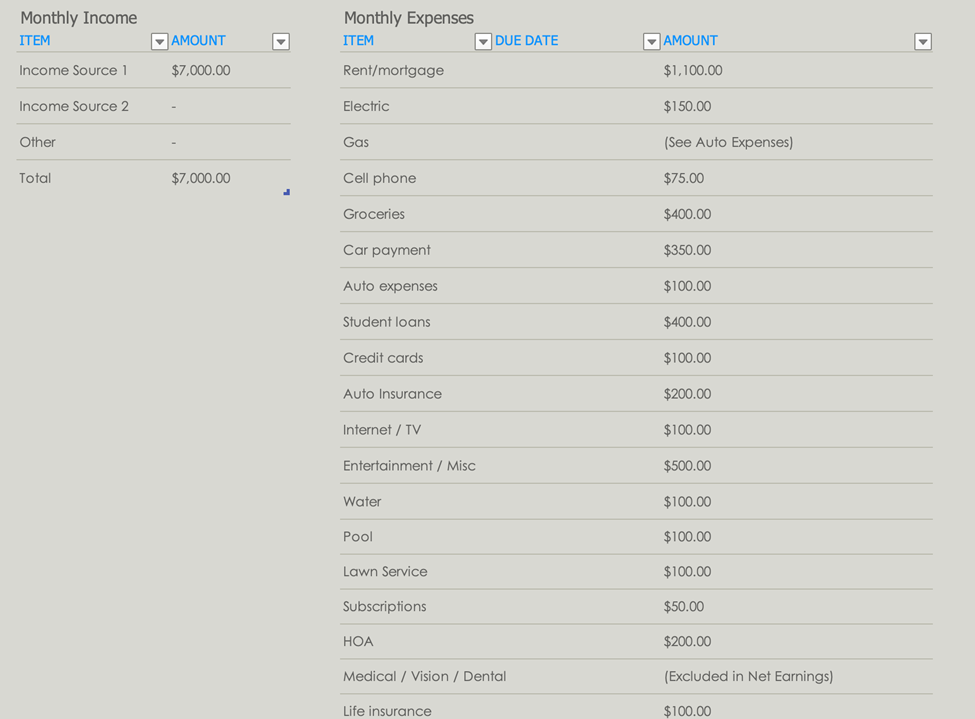

So, we have an overall view of total income versus total expenses. Let’s look at the third component of a budget next. Specifically, the categorization (or budget line items) that make up the expense details.

Here, we see where the expenses are allocated.

In setting up your very first budget, you will most likely fill in the applicable areas with what you are currently paying. This would be to create a baseline of spending and determine what your current situation looks like.

Ideally, you want to get to a point where you “set” the amounts you want to allocate to each line item, and then decide if you need to change something (e.g., your cable provider) to fit that bill into your line-item limit.

For example, under the “internet / tv” budget line item, you can choose to only allocate $100. If your current charge each month is $150, then you can either make an adjustment elsewhere, or shop for a different service to push that amount down to $100 which is your limit for this.

Another common misconception I often hear around setting up a budget, is that there are “one off” or unplanned expenses, and a budget doesn’t handle those appropriately. The way to deal with this is the following:

1) There are very rarely instances of unforeseen expenses. For example:

- You know Christmas or equivalent holiday occurs each year at a certain time

- You know “so and so’s” birthday is “x” date

- You know about that vacation trip you scheduled with your friends a few months out

- If there is an unforeseen medical cost, you can either draw down from miscellaneous or at the worst, borrow from savings if the costs are significant

In these cases, beforehand, you boost your miscellaneous budget line item to account for it.

Consideration: think of this line item as a reserve of sorts, a catch-all bucket that would cover these types of unplanned or non-routine type of spending instances. Just be sure to manage the miscellaneous line item accordingly, and do not use it as a personal slush fund, and it will work for you as designed.

Let’s now address the restrictions (or perceived) on budgets.

Budgets are not entirely rigid. It’s your money – you spend it where you want to. Now, you may not be able to spend whatever you want on everything you want, but then your earnings come into question. This is where your desired lifestyle should be considered.

The idea here is that a budget is what you set it up to be. It allows you the flexibility to assign specific amounts to specific expenses and manage those expenses against those limits. That’s all. If you want to spend more money on entertainment and personal care, then if you are hitting your savings’ target, you just need to change something else in your budget to allow for the increase in spending under entertainment.

We’ve all balanced a checkbook, right? The point in this exercise is to balance the overall expenses compared to total earnings, all the while your key savings targets being hit consistently each month.

As much as we all think we can do the monthly accounting in our heads in terms of the amount of money going out the door, we are kidding ourselves. Look at your checking account transactions over the last month, and I guarantee there are a handful of charges you won’t even remember and will need to check further to recall what they are. And you’ll also identify several charges that you were not even aware of – they could be small but add up!

A budget is there to not look at daily. Rather, to look back on each month and see how you are performing against it and whether you need to make any adjustments.

After all, why are we doing this in the first place? Because you have clear financial targets that allow you to hit your long-term goals. And, if you are not doing a health check on your monthly budget, your chance of hitting those targets dwindles rapidly.

In summary:

1) Establishing a budget gives you the insight as to how you will hit your future, financial targets. You need to allocate money each month to savings, and a budget preserves the integrity of that function

2) Veering off track on your monthly spending or altogether ignoring a budget will undoubtedly ensure you are making very little, if no progress toward your future goals

3) Budgets are easy and are not restrictive. It’s your money, and you get to choose where it gets spent

4) You do not need to be a calculus major to develop a budget. Templates are readily available for free online, and all you need to do is plug in your personal, financial information

- As a start, I would encourage you to visit the “resources” page on this site and download your free copy of a budget template to start using today